[SINGAPORE] As global interest in nuclear energy surges, investors can gain exposure to the sector by betting on physical uranium or miners, utilities companies and reactor manufacturers, said DBS in a report.

The bank, in the latest edition of its Chief Investment Officer Vantage Point report on Monday (Jun 16), said: “(We) believe that nuclear energy is at the cusp of a new renaissance.”

Nuclear power is gaining traction as countries face an urgent need to decarbonise, diversify energy sources amid geopolitical conflict and meet growing electricity demand with the rise of artificial intelligence (AI).

The emergence of a new class of nuclear reactors, known as small modular reactors (SMRs), is another factor. These reactors can be developed in places unsuitable for traditional nuclear plants, and at lower startup costs.

“(By) engineering and economic merit alone, nuclear power should certainly command much greater attention in the narratives of energy transition today,” said DBS in the report.

Where to invest

The most straightforward play for investors would be in physical uranium, as the growing demand for nuclear energy “unambiguously implies a growing need” for the radioactive metal.

A NEWSLETTER FOR YOU

Friday, 12.30 pm

ESG Insights

An exclusive weekly report on the latest environmental, social and governance issues.

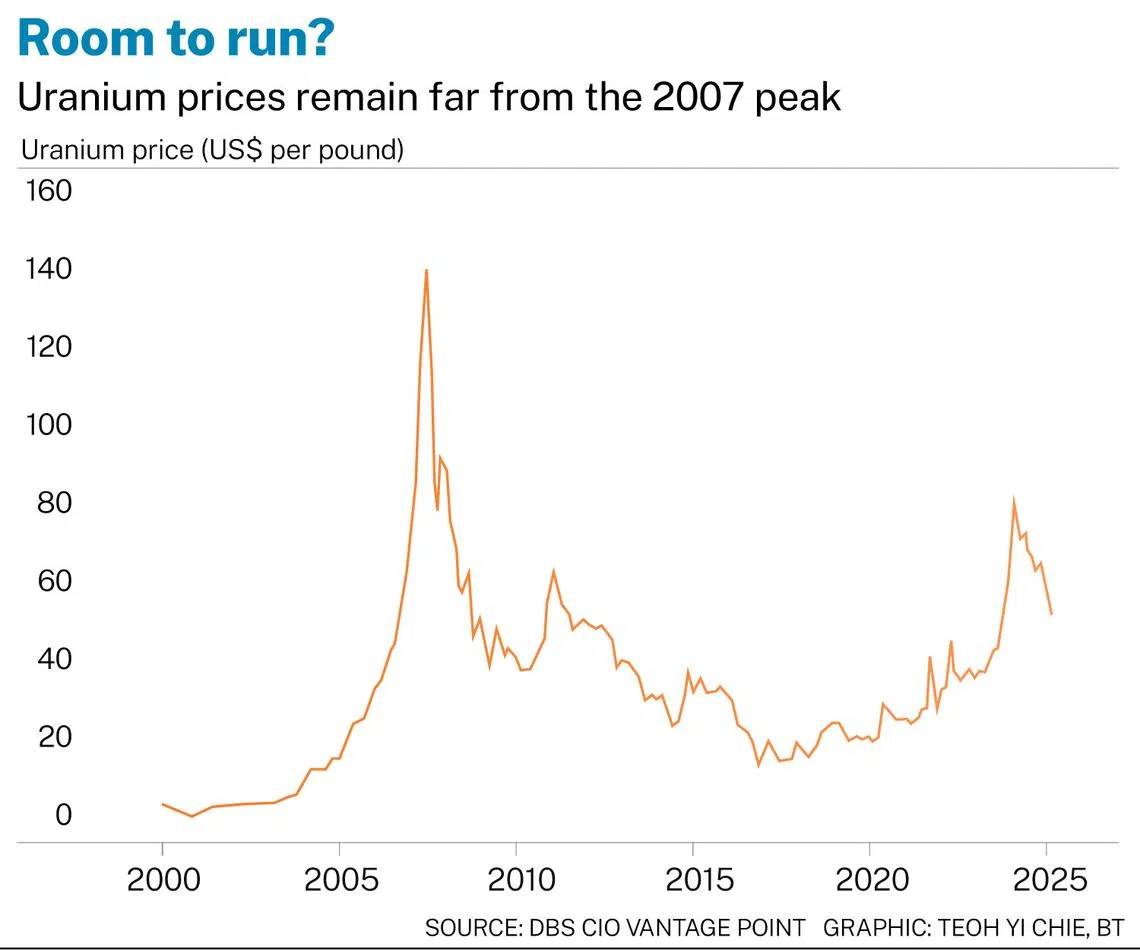

DBS noted that uranium prices have rallied over 160 per cent since the end of 2019, outperforming oil, natural gas and gold. But despite strong demand and a supply crunch, spot uranium prices remain far from their 2007 peak.

Investors can get exposure to the metal, which trades over the counter, through futures, exchange-traded funds or listed companies that hold physical uranium.

Another investment opportunity lies in uranium miners, which “would clearly be beneficiaries under a nuclear energy revolution”, said DBS.

It noted that key mining players have had strong returns between 2022 and 2024, with some outperforming the 53.2 per cent return of the S&P 500 Index during that period (see table).

While players involved in exploration and development face larger execution risks, producers generally have more predictable cash flows based on underlying commodity prices, said DBS.

Another means of exposure is through utility companies which have considerable nuclear power generation.

Independent power producers such as Vistra, Constellation and NRG Energy turned in “resilient performances” in 2024, said DBS.

This comes as data centres and big tech companies seek opportunities to procure nuclear power from such producers, spurred by the robust outlook for AI.

That said, the utilities sector is sensitive to macroeconomic factors such as interest rates and electricity demand. Another potential headwind could come from US President Donald Trump rolling back tax credits that clean-energy companies have enjoyed under the Inflation Reduction Act.

“Nonetheless, nuclear power generation continues to receive bipartisan support and could escape the fallout from proposed budget cuts, and continue to benefit from said credits,” noted DBS.

SMR growth

Nuclear reactor manufacturers are another possible play, which includes conglomerates General Electric and Rolls Royce. The latter has a proprietary design for SMRs and is set to eventually build them for sale.

DBS reckons that SMRs could follow the same “S-curve” growth trajectory of breakthrough innovations such as mobile phones and electric vehicles.

At present, the only investable SMR pure play is NuScale Power, although the company is still small and unprofitable.

Nevertheless, DBS believes that “the investable opportunities would continue to grow as more private companies working on advanced nuclear and SMR technology begin to go public”.

There is also a “plethora of opportunities” in the private market – with companies working on not just SMRs, but also the latest version of conventional nuclear reactors, known as “Gen IV reactors”.

“Breakthroughs in both safety and scalability, we believe, would precipitate a ‘tipping point’ moment in nuclear adoption, which would imply significant upside for early-stage investors in this space,” said DBS.

Moving forward

While there has been plenty of scepticism over nuclear power – especially in the wake of the 2011 Fukushima meltdown – the energy source has a promising outlook.

Contrary to popular belief, nuclear power has a good safety profile; it had just 0.03 fatalities per terawatt hour of electricity produced, noted DBS’ chief investment officer Hou Wey Fook in the report. In contrast, the fatality rates of coal and oil are 24.6 and 18.4 respectively.

Another positive for nuclear energy is its low-cost, high-energy return on investment.

That said, there are supply-chain risks with a concentration of resources in certain countries. Kazakhstan exports about 46 per cent of the world’s raw uranium, and Russia owns nearly half the world’s nuclear enrichment capacity.

There are also “well-founded” concerns over weapon proliferation, accidents and the risks of radioactive waste disposal, noted Hou.

“However, the argument for nuclear energy is not simply about who is right, but the direction the world is pushing lawmakers and corporations towards,” he said.

“Regardless of public opinion, the world moves forward,” he added.